Your contact for new licenses

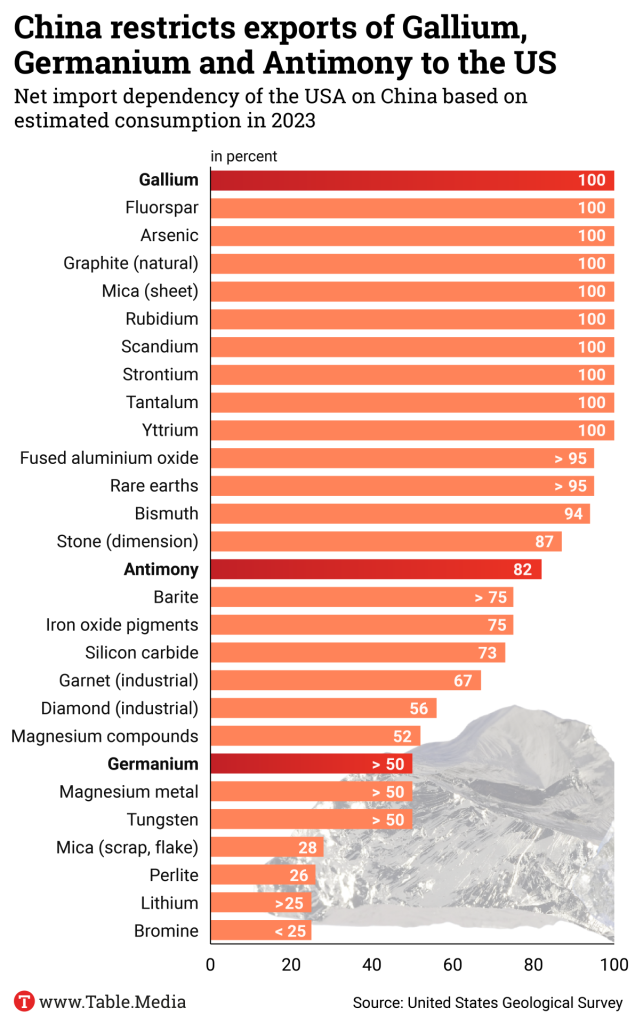

In the midst of a global supply chain upheaval and growing geopolitical tensions, the trade dispute between China and the US over strategic raw materials like gallium and germanium is coming into the spotlight. These materials are essential for key technologies, including semiconductors, batteries and renewable energies. The conflict goes far beyond the economic sphere – it is a battle for technological supremacy and geopolitical influence.

Knowing this, Beijing tightened controls on the export of these materials at the beginning of December, a move aimed at strengthening its strategic position. This has caused concern in the USA and Europe, as Jörn Petring writes. One clause could prove particularly problematic for European companies.

We hope you have a relaxing first weekend in 2025!

The Chinese Ministry of Commerce is taking a further step in the trade war over strategic raw materials with the USA: on Thursday, the Ministry presented a list of export restrictions for some technologies used to manufacture battery components and process the critical minerals lithium and gallium. Technologies for the extraction of gallium are also said to be affected. The Ministry did not specify when the restrictions could come into force.

A small but important part of the global commodities market has been in turmoil for weeks. The metals germanium and antimony have reached record highs, while gallium is more expensive than it has been for 13 years. The trigger for the skyrocketing prices has been an announcement by the Beijing Ministry of Trade in early December.

In response to new chip sanctions imposed by Washington, China announced that it would expand existing restrictions on the export of the three metals to the USA into a strict export ban. One point in particular, a transshipment clause, packs a punch: For the first time, it also prohibits companies in third countries from reselling these materials to US companies after purchasing them from China.

“The move marks a significant escalation of the ongoing tech war between the US and China, and EU businesses are increasingly worried about being caught in the crossfire,” Jens Eskelund, the president of the European Union Chamber of Commerce in China, told the New York Times.

The spokesperson for the Chinese Ministry of Commerce, He Jiandao, however, defended the new regulations as “a reasonable measure.” He said China was “willing to strengthen dialogue with all parties in the field of export controls and jointly maintain the stability and smooth flow of global production and supply chains.”

The turmoil in the US chip, aerospace and defense industries is great. According to a Bloomberg report, diverted shipments from third countries have recently been an important lifeline, particularly for gallium, an essential component for products in these industries. However, these flows could now dry up completely. After all, suppliers are now afraid of retaliatory measures from Beijing.

Even before Donald Trump moves into the White House, China demonstrates that it is increasingly willing to use its raw materials as leverage. This is the country’s response to the growing trade restrictions imposed by the US. Analysts have long warned that Beijing has a powerful weapon at its disposal thanks to its dominance in this area.

China could “coerce governments and businesses and artificially inflate prices through supply restriction – if it chose to do so,” the UBS bank warned last March: “Moves of this kind remind the West that many of its most innovative companies are still heavily dependent on Chinese-owned or processed materials for production of next-generation technologies.”

Although the United States has gallium deposits, it does not currently produce significant quantities of the metal. The extraction of gallium is expensive and was considered unprofitable in the past, especially in light of cheap Chinese imports. The People’s Republic controls around 98 percent of global gallium production and has been able to dominate the market thanks to low prices.

Although companies such as Nyrstar have plans to set up gallium and germanium production in Tennessee, these projects are still in the planning or early development phase.

Global companies are reacting quickly to Beijing’s new rules. The raw materials giant Rio Tinto senses an opportunity and wants to position itself as the savior of western gallium production. Just days after the announcement by the Chinese Ministry of Commerce, the company announced plans to set up a new gallium production facility in Canada.

The initial plan is to build a demonstration plant with a production capacity of up to 3.5 tons of gallium per year. In the long term, a commercial plant could produce up to 40 tons of gallium per year, equivalent to around five to ten percent of current global production.

However, observers fear gallium, germanium and antimony are just the beginning. After all, China has numerous options for using critical minerals as leverage. The Chinese investment bank CITIC recently warned in a statement that Beijing could extend its export controls to dozens of niche materials. It listed the 17 known rare earths and other raw materials in which China plays a dominant role as a producer or processor.

Rare earths are not really “rare” but are relatively common in the earth’s crust. However, extracting these elements in their pure form and without causing significant environmental damage is difficult. China dominates global processing and has thus gained a strategic advantage.

Although the USA could do without Chinese supplies, it would have to make massive investments to build up its own supply chains. Alongside Canada, Australia also sees opportunities. Australian media rejoice that the growing demand for alternatives to Chinese supplies could further strengthen Australia’s position as a leading exporter of raw materials.

China’s GDP growth slowed during the first three quarters of 2024, from 5.3 percent to 4.7 percent to 4.6 percent, raising fears that the country would not achieve its annual growth target of around 5 percent. But the latest data suggest that China’s economy is finally turning the corner.

Economic activity in China has been relatively weak since the COVID-19 crisis. This was not unexpected, at least not at first: three years of pandemic lockdowns strained household, corporate, and local-government balance sheets. Declining business confidence – partly a response to a regulatory crackdown on finance, the property sector, and the platform economy – did not help matters.

In early 2021, when the United States emerged from the worst of its pandemic lockdowns, American households quickly began spending the money they had accumulated. Chinese households, by contrast, continued to accumulate savings even after the lockdowns were over: between January 2020 and August 2024, household bank deposits in China swelled by 65.4 trillion RMB (9 trillion US dollars), with the wealthy accounting for a significant share.

China’s government introduced some supportive policies over this period, but in contrast to past disruptions, it refrained from implementing aggressive stimulus policies, owing to concerns about possible side effects. The massive stimulus package the government introduced after the 2008 global financial crisis spurred growth, but it also fueled a real-estate bubble, drove up local-government debt, and reduced investment efficiency.

The government’s calculations changed at the end of the third quarter of 2024, when it became clear that China’s economy would need more help to lift its growth trajectory. In late September, People’s Bank of China Governor Pan Gongsheng unveiled three measures: a reduction in banks’ reserve ratio, a policy-rate cut, and the creation of monetary-policy instruments to support the stock market.

Moreover, on October 12, Lan Fo’an, China’s finance minister, announced that new fiscal measures would focus on addressing local-government debt problems, stabilizing the real-estate market, and supporting employment. He followed this announcement in early November with a 10 trillion RMB debt-swap plan for local governments.

Both Pan and Lan have suggested that more stimulus measures are in the pipeline, with Lan noting that China’s central government still has plenty of room to increase its debt and deficits. But recent data on high-frequency economic indicators – which tend to be the quickest to respond to macroeconomic-policy changes – suggest that the government’s actions began taking effect almost immediately.

In October, total “social finance” (total financing to the real economy) was up by 7.8 percent year-on-year, and outstanding bank loans had increased by 7.7 percent. Retail sales had risen by 4.8 percent year-on-year, and by 1.6 percentage points from the previous month. The manufacturing purchasing managers’ index reached 50.1, after three months of sub-50 readings, and increased again, to 50.3, in November.

In more good news, the surveyed urban unemployment rate dropped by 0.1 percentage points in October, to 5 percent. Even the property market improved marginally, though land sales and real-estate investment remained weak. If these positive trends continue, GDP growth will probably return to around 5 percent in the fourth quarter of 2024.

The outlook for 2025, however, is less clear. If China is to achieve 5 percent GDP growth next year – assuming this is the government’s target – policymakers will have to overcome three key challenges, starting with stabilizing the property sector, which contributes about 20 percent of GDP growth and accounts for 70 percent of household wealth.

The second challenge is local governments’ balance sheets. A shortage of funds has lately been driving local authorities to cut spending, such as by reducing officials’ salaries, and grasp for revenues, such as by chasing corporate back taxes and even detaining private entrepreneurs from other regions. None of this is good for growth.

The fundamental problem is that spending responsibilities now exceed fiscal revenues, which are no longer being bolstered by land sales and local-government investment vehicles. The central government must urgently transfer a significant amount of general-purpose revenue to local authorities. More fundamentally, China needs to reconfigure the balance of fiscal responsibilities across levels of government.

The third major challenge that China will confront in 2025 is US President-elect Donald Trump, who has vowed to impose 60 percent tariffs on all imports from China during his first year in office. Given that China’s exports to the US account for 3 percent of its GDP, such tariffs – and even much lower ones – would have a material impact on growth in 2025. The investment bank UBS, for instance, predicted that China’s GDP growth would slow to 4 percent in 2025.

There has been much debate in China over whether the economy needs structural reforms or more macroeconomic stimulus. The truth is that it needs both. A decisive stimulus package, with a robust fiscal-policy component, must come first; this will make the biggest immediate difference. But once the package is in place, the government should turn its attention to structural reforms, with a focus on boosting confidence among consumers, investors, and entrepreneurs.

Over the past year, China’s government has published several policy documents aimed at restoring confidence. But with market participants not fully convinced, it must go further, implementing – boldly and visibly – some of the measures it has announced, such as stronger protections for private enterprises. Reining in local officials’ scrutiny of old tax records in search of missing payments would also go a long way toward strengthening business confidence.

Huang Yiping, Dean of the National School of Development and a professor at Peking University, is a member of the Monetary Policy Committee of the People’s Bank of China.

Copyright: Project Syndicate, 2024.

www.project-syndicate.org

Editor’s note: Discussing China today means – more than ever – engaging in controversial debate. We want to reflect the diversity of Opinions so that you can gain an insight into the breadth of the debate. Opinion articles do not reflect the opinion of the editorial team.

China declared a “toilet revolution” in 2015. The campaign aimed to increase the number of public toilets nationwide and improve their quality. This mirrored op-art toilet on the sixth floor of Deji Plaza in the city of Nanjing proves that they may have slightly over-achieved here and there. The design, reminiscent of the movie Austin Powers, was created by the Shanghai-based architecture firm X+Living.

In the midst of a global supply chain upheaval and growing geopolitical tensions, the trade dispute between China and the US over strategic raw materials like gallium and germanium is coming into the spotlight. These materials are essential for key technologies, including semiconductors, batteries and renewable energies. The conflict goes far beyond the economic sphere – it is a battle for technological supremacy and geopolitical influence.

Knowing this, Beijing tightened controls on the export of these materials at the beginning of December, a move aimed at strengthening its strategic position. This has caused concern in the USA and Europe, as Jörn Petring writes. One clause could prove particularly problematic for European companies.

We hope you have a relaxing first weekend in 2025!

The Chinese Ministry of Commerce is taking a further step in the trade war over strategic raw materials with the USA: on Thursday, the Ministry presented a list of export restrictions for some technologies used to manufacture battery components and process the critical minerals lithium and gallium. Technologies for the extraction of gallium are also said to be affected. The Ministry did not specify when the restrictions could come into force.

A small but important part of the global commodities market has been in turmoil for weeks. The metals germanium and antimony have reached record highs, while gallium is more expensive than it has been for 13 years. The trigger for the skyrocketing prices has been an announcement by the Beijing Ministry of Trade in early December.

In response to new chip sanctions imposed by Washington, China announced that it would expand existing restrictions on the export of the three metals to the USA into a strict export ban. One point in particular, a transshipment clause, packs a punch: For the first time, it also prohibits companies in third countries from reselling these materials to US companies after purchasing them from China.

“The move marks a significant escalation of the ongoing tech war between the US and China, and EU businesses are increasingly worried about being caught in the crossfire,” Jens Eskelund, the president of the European Union Chamber of Commerce in China, told the New York Times.

The spokesperson for the Chinese Ministry of Commerce, He Jiandao, however, defended the new regulations as “a reasonable measure.” He said China was “willing to strengthen dialogue with all parties in the field of export controls and jointly maintain the stability and smooth flow of global production and supply chains.”

The turmoil in the US chip, aerospace and defense industries is great. According to a Bloomberg report, diverted shipments from third countries have recently been an important lifeline, particularly for gallium, an essential component for products in these industries. However, these flows could now dry up completely. After all, suppliers are now afraid of retaliatory measures from Beijing.

Even before Donald Trump moves into the White House, China demonstrates that it is increasingly willing to use its raw materials as leverage. This is the country’s response to the growing trade restrictions imposed by the US. Analysts have long warned that Beijing has a powerful weapon at its disposal thanks to its dominance in this area.

China could “coerce governments and businesses and artificially inflate prices through supply restriction – if it chose to do so,” the UBS bank warned last March: “Moves of this kind remind the West that many of its most innovative companies are still heavily dependent on Chinese-owned or processed materials for production of next-generation technologies.”

Although the United States has gallium deposits, it does not currently produce significant quantities of the metal. The extraction of gallium is expensive and was considered unprofitable in the past, especially in light of cheap Chinese imports. The People’s Republic controls around 98 percent of global gallium production and has been able to dominate the market thanks to low prices.

Although companies such as Nyrstar have plans to set up gallium and germanium production in Tennessee, these projects are still in the planning or early development phase.

Global companies are reacting quickly to Beijing’s new rules. The raw materials giant Rio Tinto senses an opportunity and wants to position itself as the savior of western gallium production. Just days after the announcement by the Chinese Ministry of Commerce, the company announced plans to set up a new gallium production facility in Canada.

The initial plan is to build a demonstration plant with a production capacity of up to 3.5 tons of gallium per year. In the long term, a commercial plant could produce up to 40 tons of gallium per year, equivalent to around five to ten percent of current global production.

However, observers fear gallium, germanium and antimony are just the beginning. After all, China has numerous options for using critical minerals as leverage. The Chinese investment bank CITIC recently warned in a statement that Beijing could extend its export controls to dozens of niche materials. It listed the 17 known rare earths and other raw materials in which China plays a dominant role as a producer or processor.

Rare earths are not really “rare” but are relatively common in the earth’s crust. However, extracting these elements in their pure form and without causing significant environmental damage is difficult. China dominates global processing and has thus gained a strategic advantage.

Although the USA could do without Chinese supplies, it would have to make massive investments to build up its own supply chains. Alongside Canada, Australia also sees opportunities. Australian media rejoice that the growing demand for alternatives to Chinese supplies could further strengthen Australia’s position as a leading exporter of raw materials.

China’s GDP growth slowed during the first three quarters of 2024, from 5.3 percent to 4.7 percent to 4.6 percent, raising fears that the country would not achieve its annual growth target of around 5 percent. But the latest data suggest that China’s economy is finally turning the corner.

Economic activity in China has been relatively weak since the COVID-19 crisis. This was not unexpected, at least not at first: three years of pandemic lockdowns strained household, corporate, and local-government balance sheets. Declining business confidence – partly a response to a regulatory crackdown on finance, the property sector, and the platform economy – did not help matters.

In early 2021, when the United States emerged from the worst of its pandemic lockdowns, American households quickly began spending the money they had accumulated. Chinese households, by contrast, continued to accumulate savings even after the lockdowns were over: between January 2020 and August 2024, household bank deposits in China swelled by 65.4 trillion RMB (9 trillion US dollars), with the wealthy accounting for a significant share.

China’s government introduced some supportive policies over this period, but in contrast to past disruptions, it refrained from implementing aggressive stimulus policies, owing to concerns about possible side effects. The massive stimulus package the government introduced after the 2008 global financial crisis spurred growth, but it also fueled a real-estate bubble, drove up local-government debt, and reduced investment efficiency.

The government’s calculations changed at the end of the third quarter of 2024, when it became clear that China’s economy would need more help to lift its growth trajectory. In late September, People’s Bank of China Governor Pan Gongsheng unveiled three measures: a reduction in banks’ reserve ratio, a policy-rate cut, and the creation of monetary-policy instruments to support the stock market.

Moreover, on October 12, Lan Fo’an, China’s finance minister, announced that new fiscal measures would focus on addressing local-government debt problems, stabilizing the real-estate market, and supporting employment. He followed this announcement in early November with a 10 trillion RMB debt-swap plan for local governments.

Both Pan and Lan have suggested that more stimulus measures are in the pipeline, with Lan noting that China’s central government still has plenty of room to increase its debt and deficits. But recent data on high-frequency economic indicators – which tend to be the quickest to respond to macroeconomic-policy changes – suggest that the government’s actions began taking effect almost immediately.

In October, total “social finance” (total financing to the real economy) was up by 7.8 percent year-on-year, and outstanding bank loans had increased by 7.7 percent. Retail sales had risen by 4.8 percent year-on-year, and by 1.6 percentage points from the previous month. The manufacturing purchasing managers’ index reached 50.1, after three months of sub-50 readings, and increased again, to 50.3, in November.

In more good news, the surveyed urban unemployment rate dropped by 0.1 percentage points in October, to 5 percent. Even the property market improved marginally, though land sales and real-estate investment remained weak. If these positive trends continue, GDP growth will probably return to around 5 percent in the fourth quarter of 2024.

The outlook for 2025, however, is less clear. If China is to achieve 5 percent GDP growth next year – assuming this is the government’s target – policymakers will have to overcome three key challenges, starting with stabilizing the property sector, which contributes about 20 percent of GDP growth and accounts for 70 percent of household wealth.

The second challenge is local governments’ balance sheets. A shortage of funds has lately been driving local authorities to cut spending, such as by reducing officials’ salaries, and grasp for revenues, such as by chasing corporate back taxes and even detaining private entrepreneurs from other regions. None of this is good for growth.

The fundamental problem is that spending responsibilities now exceed fiscal revenues, which are no longer being bolstered by land sales and local-government investment vehicles. The central government must urgently transfer a significant amount of general-purpose revenue to local authorities. More fundamentally, China needs to reconfigure the balance of fiscal responsibilities across levels of government.

The third major challenge that China will confront in 2025 is US President-elect Donald Trump, who has vowed to impose 60 percent tariffs on all imports from China during his first year in office. Given that China’s exports to the US account for 3 percent of its GDP, such tariffs – and even much lower ones – would have a material impact on growth in 2025. The investment bank UBS, for instance, predicted that China’s GDP growth would slow to 4 percent in 2025.

There has been much debate in China over whether the economy needs structural reforms or more macroeconomic stimulus. The truth is that it needs both. A decisive stimulus package, with a robust fiscal-policy component, must come first; this will make the biggest immediate difference. But once the package is in place, the government should turn its attention to structural reforms, with a focus on boosting confidence among consumers, investors, and entrepreneurs.

Over the past year, China’s government has published several policy documents aimed at restoring confidence. But with market participants not fully convinced, it must go further, implementing – boldly and visibly – some of the measures it has announced, such as stronger protections for private enterprises. Reining in local officials’ scrutiny of old tax records in search of missing payments would also go a long way toward strengthening business confidence.

Huang Yiping, Dean of the National School of Development and a professor at Peking University, is a member of the Monetary Policy Committee of the People’s Bank of China.

Copyright: Project Syndicate, 2024.

www.project-syndicate.org

Editor’s note: Discussing China today means – more than ever – engaging in controversial debate. We want to reflect the diversity of Opinions so that you can gain an insight into the breadth of the debate. Opinion articles do not reflect the opinion of the editorial team.

China declared a “toilet revolution” in 2015. The campaign aimed to increase the number of public toilets nationwide and improve their quality. This mirrored op-art toilet on the sixth floor of Deji Plaza in the city of Nanjing proves that they may have slightly over-achieved here and there. The design, reminiscent of the movie Austin Powers, was created by the Shanghai-based architecture firm X+Living.